The Military Lending Act Protects the Military Community

The Military Lending Act Protects the Military CommunityThe Military Lending Act (MLA) is a legal protection that exists to protect servicemembers from predatory financial practices.

Advertising Disclosure.Advertiser Disclosure: The Military Wallet and Three Creeks Media, LLC, its parent and affiliate companies, may receive compensation through advertising placements on The Military Wallet. For any rankings or lists on this site, The Military Wallet may receive compensation from the companies being ranked; however, this compensation does not affect how, where, and in what order products and companies appear in the rankings and lists. If a ranking or list has a company noted to be a “partner,” the indicated company is a corporate affiliate of The Military Wallet. No tables, rankings, or lists are fully comprehensive and do not include all companies or available products.

The Military Wallet and Three Creeks Media have partnered with CardRatings for our coverage of credit card products. The Military Wallet and CardRatings may receive a commission from card issuers.

Opinions, reviews, analyses & recommendations are the author’s alone and have not been reviewed, endorsed, or approved by any of these entities. For more information, please see our Advertising Policy .

American Express is an advertiser on The Military Wallet. Terms Apply to American Express benefits and offers.

When service members risk their lives safeguarding our country, it is our country’s job to safeguard them. Unfortunately, the military community often finds itself targets of predatory financial entities.

In 2006, the government stepped in to safeguard the finances of military members and their families. In the sea of resources for the military community, the Military Lending Act (MLA) is a legal protection that exists whether you are aware of it or not. The most prominent feature of the Military lending Act is a 36% interest-rate cap on most consumer loans.

The Military Lending Act Protects the Military CommunityHow often do you read the fine print of contracts? What is the interest-rate cap for consumer loans for military members and their dependents?

Don’t feel bad if you aren’t confident with your answers to the questions above. That is exactly where the MLA comes in.

The Consumer Finance Protection Bureau (CPFB), an organization entirely dedicated to creating bright lines of clarity in lending, offers a host of information on fair practices and resources for consumers on lending in a general capacity. It is vital for all citizens to learn what allowances and limits are normal versus excessive. This resource is your starting line.

Select a VA Home Loan Option to Continue:

Explore My Options

Essentially, the MLA ensures that service members and their dependents don’t fall victim to outrageous interest rates, charges or provisions associated with lending.

A 36% annual interest cap military annual percentage rate (MAPR) is applied to the following:

Credit-related situations are rarely pleasant, especially for non-local military members or their families who rely on the integrity of a business to provide a fair deal. The MLA was created to both educate the military community and ensure predatory lending practices become a thing of the past.

Your local JAG office is the best place to go for advice, as well as to determine whether your personal situation falls under the ark of coverage. Active duty is generally the key phrase to look for when determining coverage.

The following members are eligible for protections under the MLA:

In order to qualify on active duty, you must have been in an active-duty status for over 30 days.

While it may seem complicated, the MLA was designed to protect military consumers in an effort to keep the force financially ready. A strong home front has always been the key to mission readiness and success for military members worldwide.

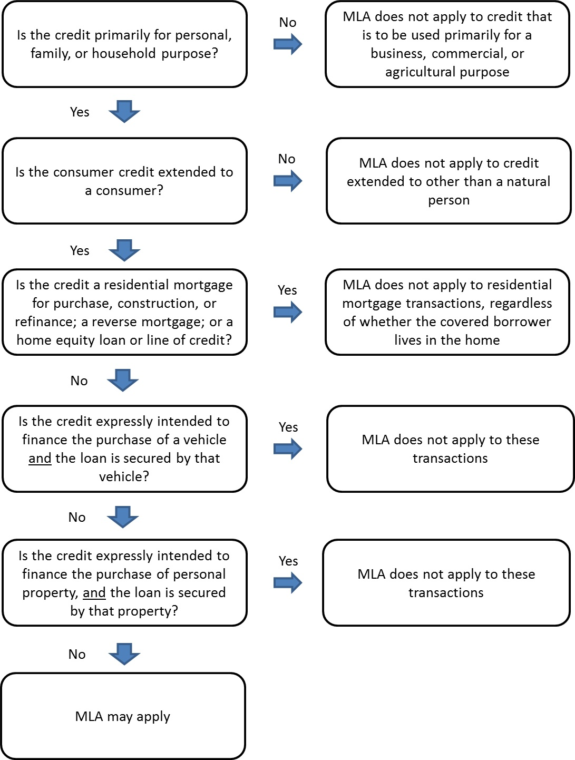

The National Credit Union Administration (NCUA) created a helpful flowchart (source) to aid military members in determining if their situation may be covered under the act. In all instances, consumer awareness remains the underlying and critical component of all financial transactions. Know your rights and benefits, and maintain an accurate and detailed record of all transactions.

Check your VA Home Loan eligibility and get personalized rates. Answer a few questions and we'll connect you with a trusted VA lender to answer any questions you have about the VA loan program.

Unfortunately, the list of what is not covered is longer than what is. Lending situations expressly covered under the MLA include:

The bulk of these scenarios are preventative coverage loans that use collateral, like a vehicle’s title or regularly occurring paychecks, to cover the loan at a higher interest rate. Remember to carefully research companies that offer these types of loans.

Eligibility under the MLA guidelines is perhaps one of the most important fine print outlines consumers need to read in full.

The MLA does not cover loans that relate to the procurement of property, such as a home or car. Examples include:

Though not expressly a benefit from the MLA, many credit card companies interpret the MLA in such a way as to waive annual credit card fees for military members and their qualifying dependents.

These include major credit card issuers, such as Chase Bank and American Express, both of which waive annual credit card fees, even for some of their more popular travel cards. Some of those cards carry annual fees that would otherwise run several hundred dollars per year and provide similar value in benefits to cardholders each year. Some of the perks can include free airport lounge access, annual travel credits, excellent rewards on purchases and much more.

Samantha Peterson is a regular contributor for military publications such as The Military Wallet, Military Families Magazine, We Are The Mighty and more. She feels passionately about telling compelling stories and crafting captivating narratives. Living life one PCS at a time, she’s travel schooling her children while tackling careers in the nonprofit and environmental sector all as military life allows.

Featured In: Samantha’s writing has been featured in We Are The Mighty, Military Families Magazine, InDependent, Reserve + National Guard Magazine, and other publications.

About the comments on this site:

These responses are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser’s responsibility to ensure all posts and/or questions are answered.

Explore Our Site:

© Three Creeks Media, LLC 2024. All Rights Reserved.

Presented by Mortgage Research Center, LLC. A mortgage licensee. NMLS ID 1907. Equal Housing Lender.

The Military Wallet is a property of Three Creeks Media. Neither The Military Wallet nor Three Creeks Media are associated with or endorsed by the U.S. Departments of Defense or Veterans Affairs. The content on The Military Wallet is produced by Three Creeks Media, its partners, affiliates and contractors, any opinions or statements on The Military Wallet should not be attributed to the Dept. of Veterans Affairs, the Dept. of Defense or any governmental entity. If you have questions about Veteran programs offered through or by the Dept. of Veterans Affairs, please visit their website at va.gov. The content offered on The Military Wallet is for general informational purposes only and may not be relevant to any consumer’s specific situation, this content should not be construed as legal or financial advice. If you have questions of a specific nature consider consulting a financial professional, accountant or attorney to discuss. References to third-party products, rates and offers may change without notice.

Advertiser Disclosure: The Military Wallet and Three Creeks Media, LLC, its parent and affiliate companies, may receive compensation through advertising placements on The Military Wallet. For any rankings or lists on this site, The Military Wallet may receive compensation from the companies being ranked; however, this compensation does not affect how, where, and in what order products and companies appear in the rankings and lists. If a ranking or list has a company noted to be a “partner,” the indicated company is a corporate affiliate of The Military Wallet. No tables, rankings, or lists are fully comprehensive and do not include all companies or available products.

Editorial Disclosure: Editorial content on The Military Wallet may include opinions. Any opinions are those of the author alone, and not those of an advertiser to the site nor of The Military Wallet.

Information from your device can be used to personalize your ad experience.